Jewelry ecommerce trends for 2026 reveal an $85.7 billion market shaped by social commerce growth, lab-grown diamonds, rising metal costs, and shifting consumer behavior toward self-purchasing.

Published:

April 19, 2026

Author:

Yi Cui

Jewelry ecommerce is growing, but the stores winning in 2026 are not just following fashion trends. They are adapting to higher metal costs, social commerce discovery, trust-heavy buying journeys, and a consumer shift toward personal, expressive jewelry.

| Metric | Benchmark | Source |

|---|---|---|

| Global online jewelry market size | $85.7 billion (2026 est.) | [360iResearch via Icecartel][1] |

| Market CAGR (2024–2030 forecast) | 13.08% | [360iResearch via Icecartel][1] |

| Online share of total jewelry sales | ~25% | [Icecartel][1] |

| Average ecommerce conversion rate (jewelry) | 1.19% – 1.5% | [Photta/WisePIM][2] [3] |

| Average Order Value — fashion jewelry | $40 – $85 | [Branvas][4] |

| Average Order Value — fine/demi-fine jewelry | $250 – $2,500+ | [Branvas][4] |

| Average return rate (jewelry ecommerce) | 16.9% – 20% | [WisePIM / Dynamic Yield][3] [5] |

| TikTok Shop jewelry GMV growth (YoY) | +94% (2025) | [Amra & Elma][6] |

| Lab-grown diamond market share (fine jewelry) | 45%+ of engagement rings | [Tenoris via National Jeweler][7] |

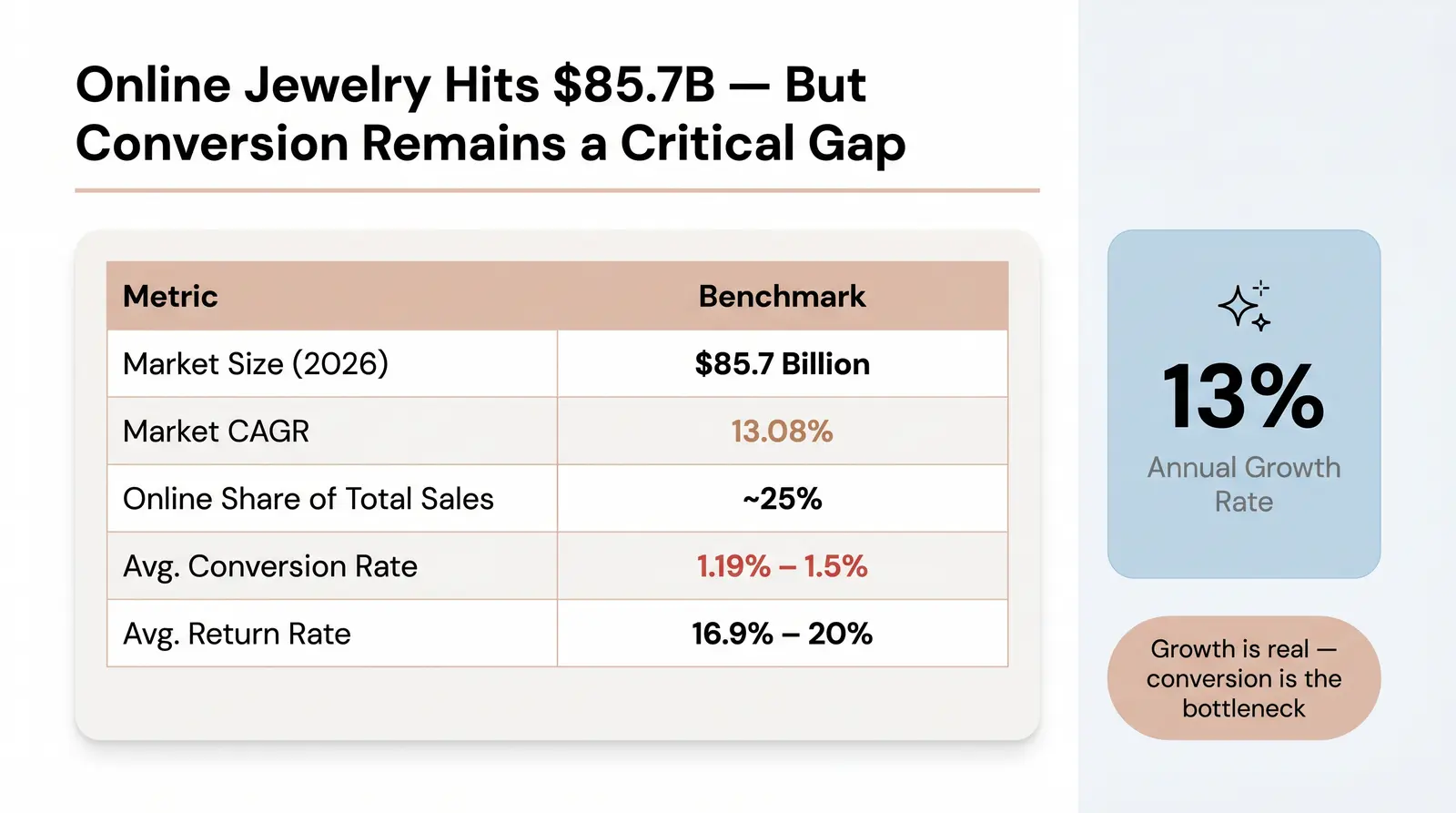

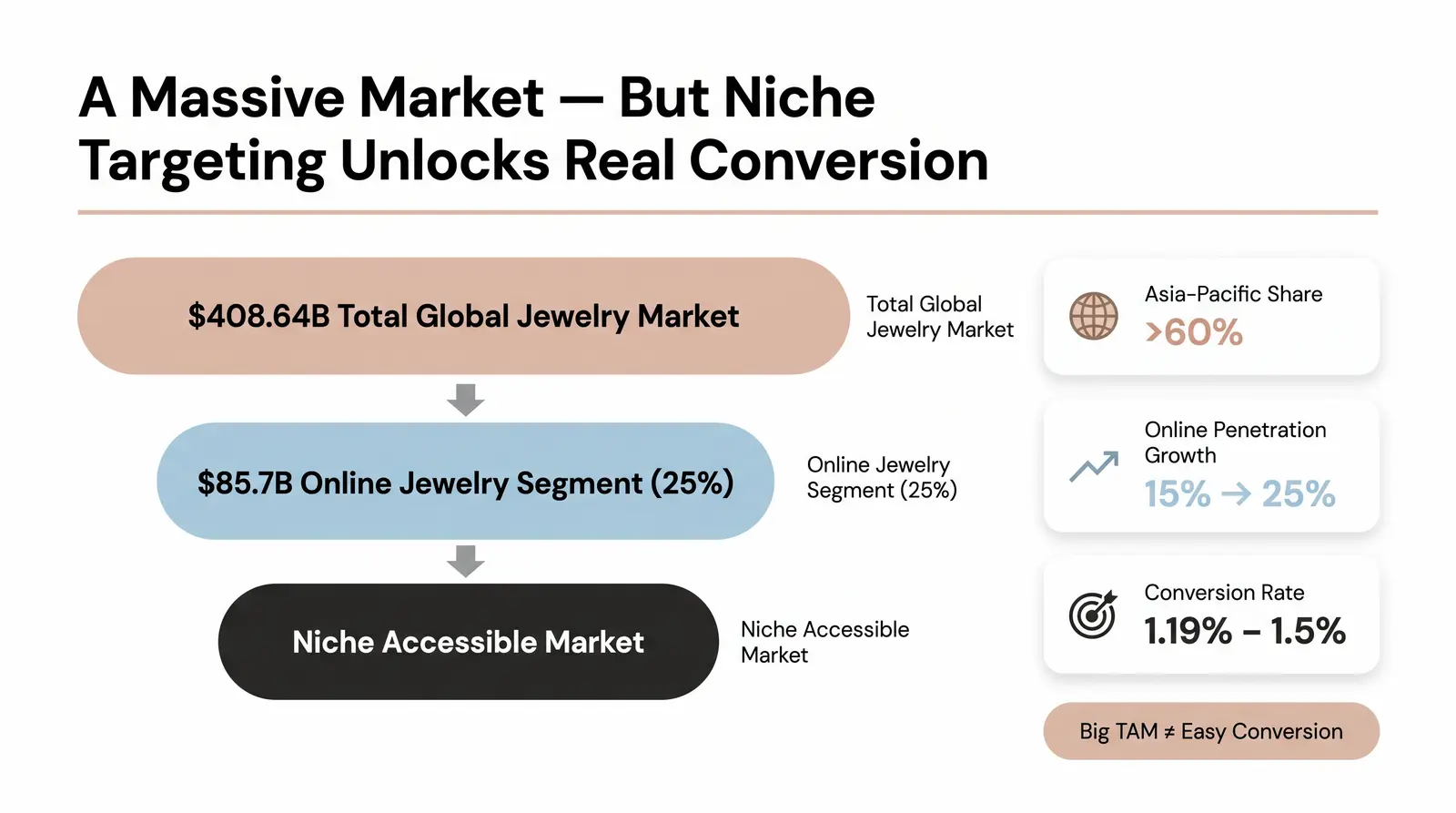

The global jewelry market is expanding rapidly, with projections placing it at $408.64 billion in 2026 and growing at a CAGR of 5.5% [8]. However, the online segment is outpacing the broader market. The global online jewelry market is projected to reach $85.7 billion in 2026, reflecting a robust 13% CAGR [1]. Online penetration has accelerated significantly, now accounting for approximately 25% of total jewelry sales, up from under 15% just five years ago [4].

Regionally, Asia-Pacific remains the powerhouse, holding over 60% of the total market share, driven by a rising middle class and strong cultural affinity for gold [8]. North America follows, fueled by high e-commerce adoption and a notable shift toward self-purchasing among younger demographics [8].

Despite these impressive top-line numbers, operators must be cautious. The headline market size figures can be misleading because they conflate gross merchandise value with the accessible market for independent brands. The reality is that the average ecommerce conversion rate for jewelry sits between 1.19% and 1.5%, the lowest of any tracked retail category [2] [3].

At Branvas, we track these macro numbers carefully — but what we've found is that the founders who scale fastest are often operating in niches that the headline market size reports don't segment clearly. They understand that a massive total addressable market doesn't guarantee a high conversion rate without deep trust and targeted merchandising.

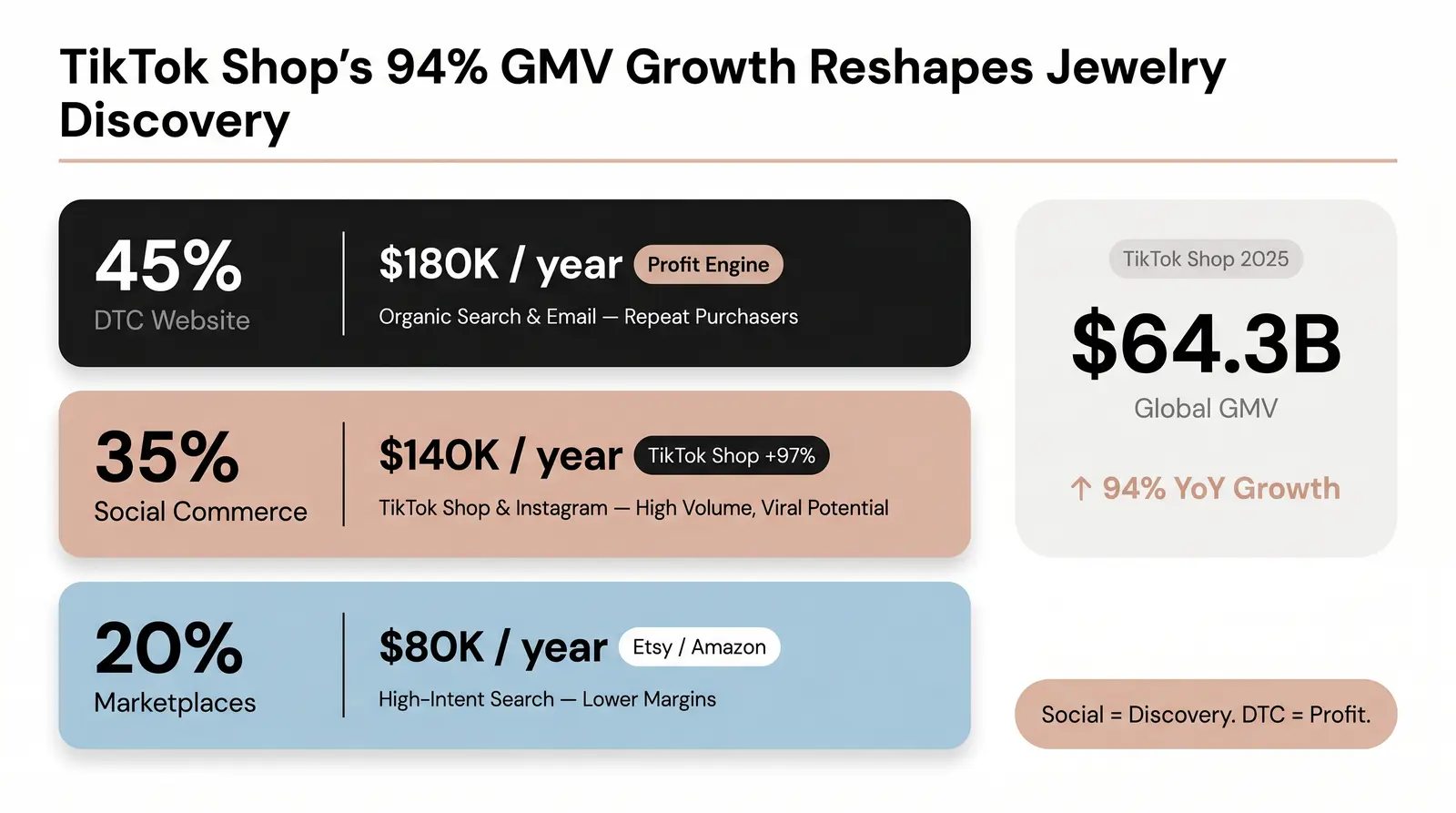

The channel mix for jewelry ecommerce has shifted sharply from traditional DTC websites to a fragmented landscape dominated by social commerce and marketplaces. While DTC remains the anchor for brand identity and high-LTV customers, discovery has moved almost entirely to social platforms.

TikTok Shop has emerged as a serious ecommerce channel, not just a trend. In 2025, global TikTok Shop GMV reached $64.3 billion, a 94% year-over-year increase [9]. For jewelry specifically, the platform has become a massive driver of impulse purchases and trend adoption. Brands generating over $30 million in revenue saw their TikTok Shop sales jump 97% year-over-year in 2025 [10].

Instagram and Pinterest play different but equally vital roles. Instagram remains the primary visual portfolio for brands, driving discovery and trust through influencer partnerships and aesthetic curation. Pinterest, however, is the engine for high-intent discovery. Users on Pinterest are actively planning purchases, making it a critical channel for bridal and milestone gifting.

Mobile commerce now dominates the transaction phase, accounting for over 60% of online jewelry purchases [1]. However, a significant portion of high-value fine jewelry purchases still close on desktop, as consumers prefer a larger screen to scrutinize details and certifications before committing to a $1,000+ purchase.

A Worked Example: Channel Mix for a $400K/Year Shopify Jewelry Store

Consider a hypothetical demi-fine jewelry brand generating $400,000 annually. In 2026, their channel revenue mix typically looks like this:

Understanding jewelry ecommerce benchmarks requires segmenting by price point and product type. The global average conversion rate of 1.5% is skewed by high-ticket fine jewelry [3].

Average Order Value (AOV) also varies wildly. The luxury and jewelry category commands the highest AOV in e-commerce, averaging $180 to $313 [4] [5]. Social commerce channels tend to drive lower AOVs ($45–$85) driven by impulse buys, while DTC channels capture higher AOVs through bundled sets and fine jewelry investments.

Return rates in jewelry average around 16.9% to 20%, which is slightly higher than the broader ecommerce average of 17.5% [3] [4]. While jewelry returns are lower than apparel (which often exceeds 30%), they are driven by different factors: ring sizing issues, color mismatch (especially with gemstones), and gifting misalignment.

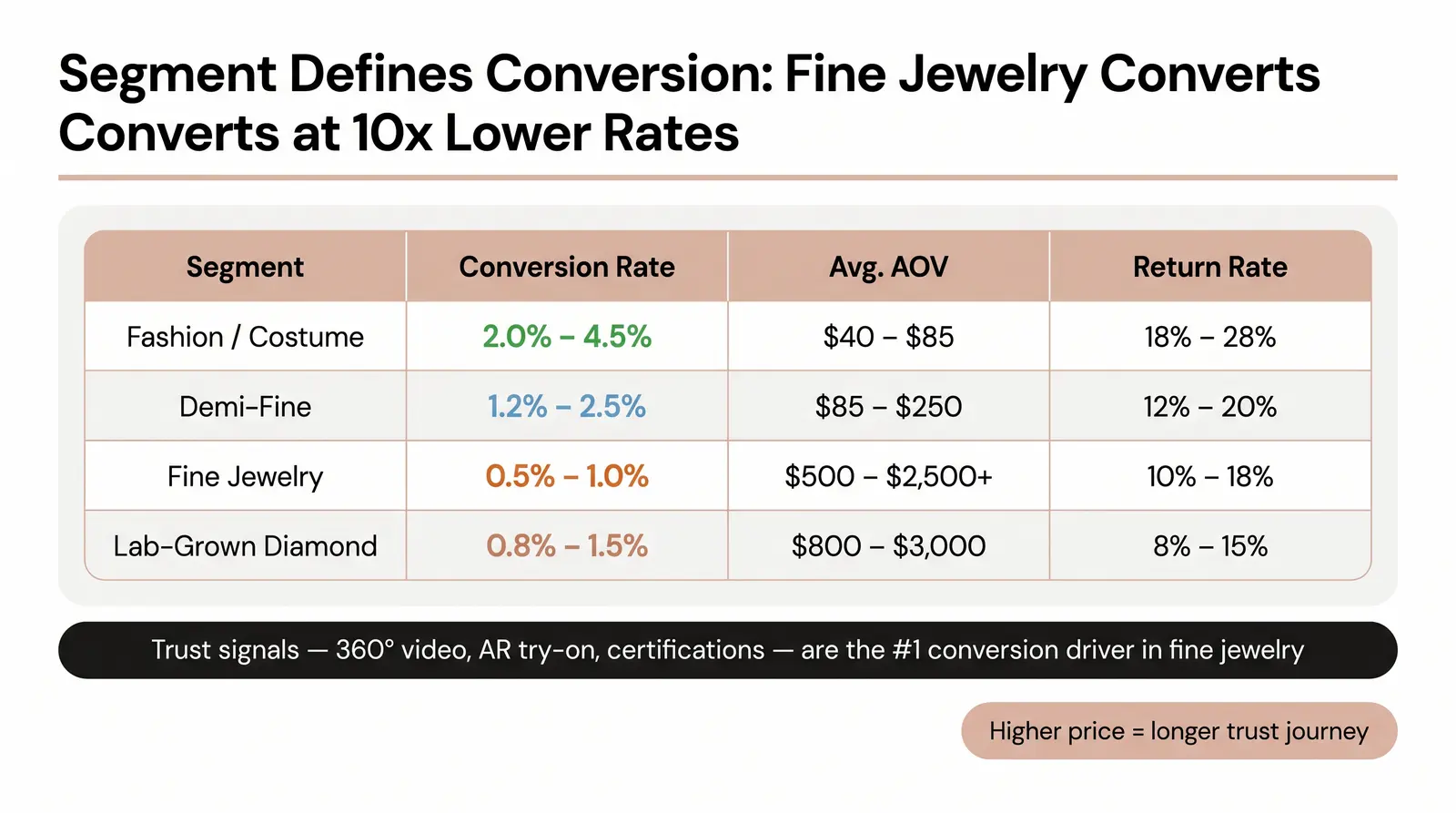

What actually moves the conversion rate in jewelry? Trust signals. Because buyers cannot physically inspect the piece, high-resolution photography, 360-degree videos, AR try-on features, detailed material specifications, and robust review volumes are non-negotiable table stakes.

Jewelry Ecommerce Benchmarks by Segment (2025–2026)

| Segment | Avg. Conversion Rate | Avg. AOV | Avg. Return Rate | Key Conversion Driver |

|---|---|---|---|---|

| Fashion/Costume Jewelry | 2.0% – 4.5% | $40 – $85 | 18% – 28% | Trend relevance, social proof, low price |

| Demi-Fine Jewelry | 1.2% – 2.5% | $85 – $250 | 12% – 20% | Material transparency, stackability, everyday wear |

| Fine Jewelry | 0.5% – 1.0% | $500 – $2,500+ | 10% – 18% | Trust signals, certifications, retargeting |

| Lab-Grown Diamond Jewelry | 0.8% – 1.5% | $800 – $3,000 | 8% – 15% | Price comparison vs. mined, ethical messaging |

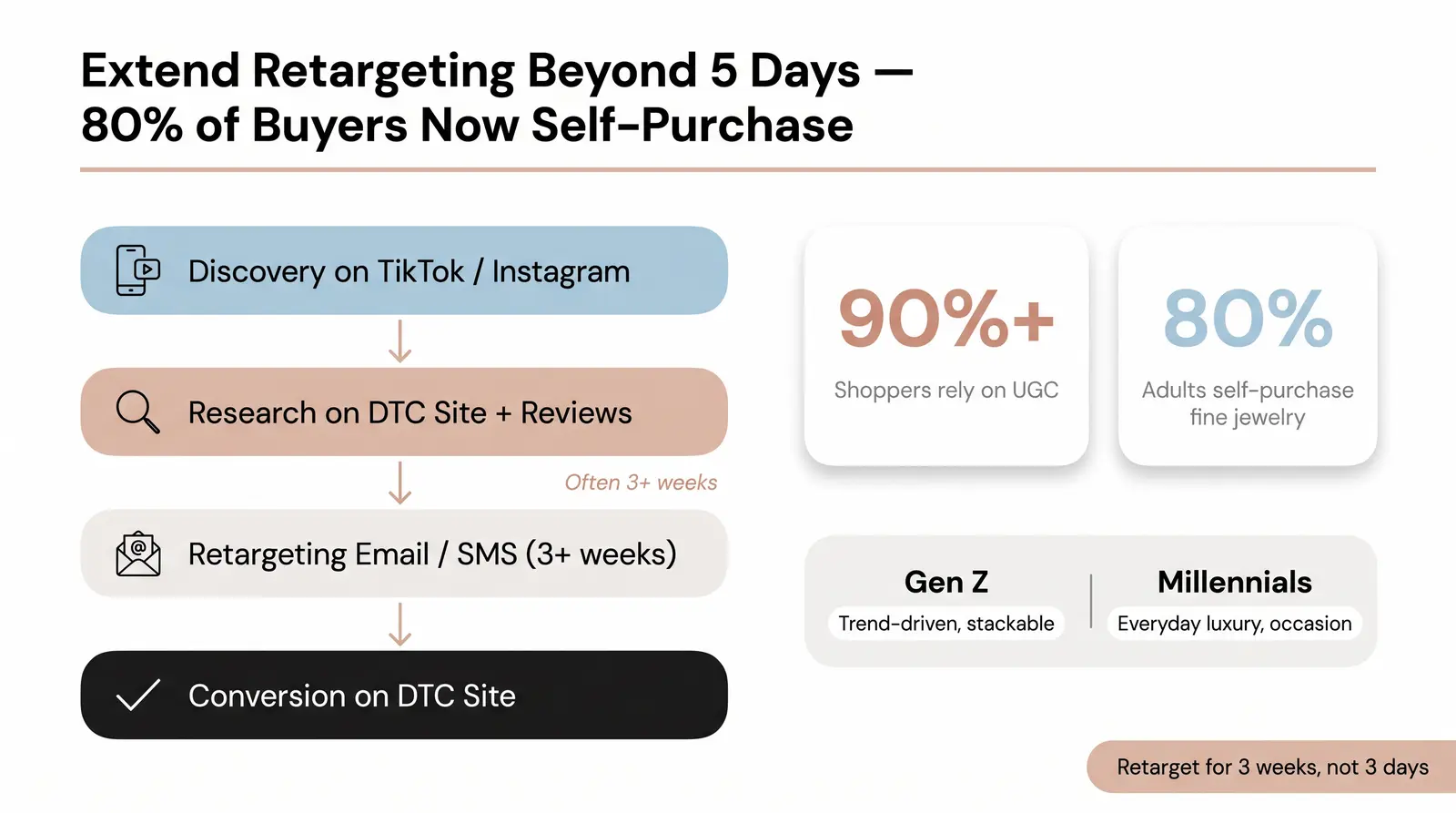

The modern jewelry buying journey is trust-heavy and increasingly complex. For fine and demi-fine pieces, the consideration phase is long. Consumers require multiple touchpoints—from initial discovery on TikTok to deep research on a DTC site, reading reviews, and finally converting via a retargeting email.

We often see founders underestimate how long a jewelry purchase decision actually takes — especially for anything over $80. Email and retargeting sequences built for 3–5 day windows frequently miss the buyer who's been considering for 3 weeks.

User-Generated Content (UGC) and peer reviews are now critical. Over 90% of jewelry shoppers consider UGC when making purchase decisions [6]. Buyers want to see how a piece looks on real people, in natural lighting, before committing.

There is also a significant shift in who is buying. While gifting remains the primary revenue driver during Q4 and holidays, self-purchasing is exploding. 80% of American adults are now more likely to buy fine jewelry for themselves rather than wait for it as a gift [4].

Generational differences are stark. Gen Z favors expressive, stackable, and trend-driven fashion jewelry, heavily influenced by social media. Millennials, entering their peak earning years, are driving the demi-fine and fine jewelry markets, seeking occasion pieces and investment items that balance quality with accessible luxury. This creates a tension in the market between "quiet luxury" (minimalist, high-quality materials) and "maximalist expression" (chunky, colorful, layered looks).

Several key product trends are defining the 2026 jewelry landscape, driven by both consumer preference and macroeconomic pressures.

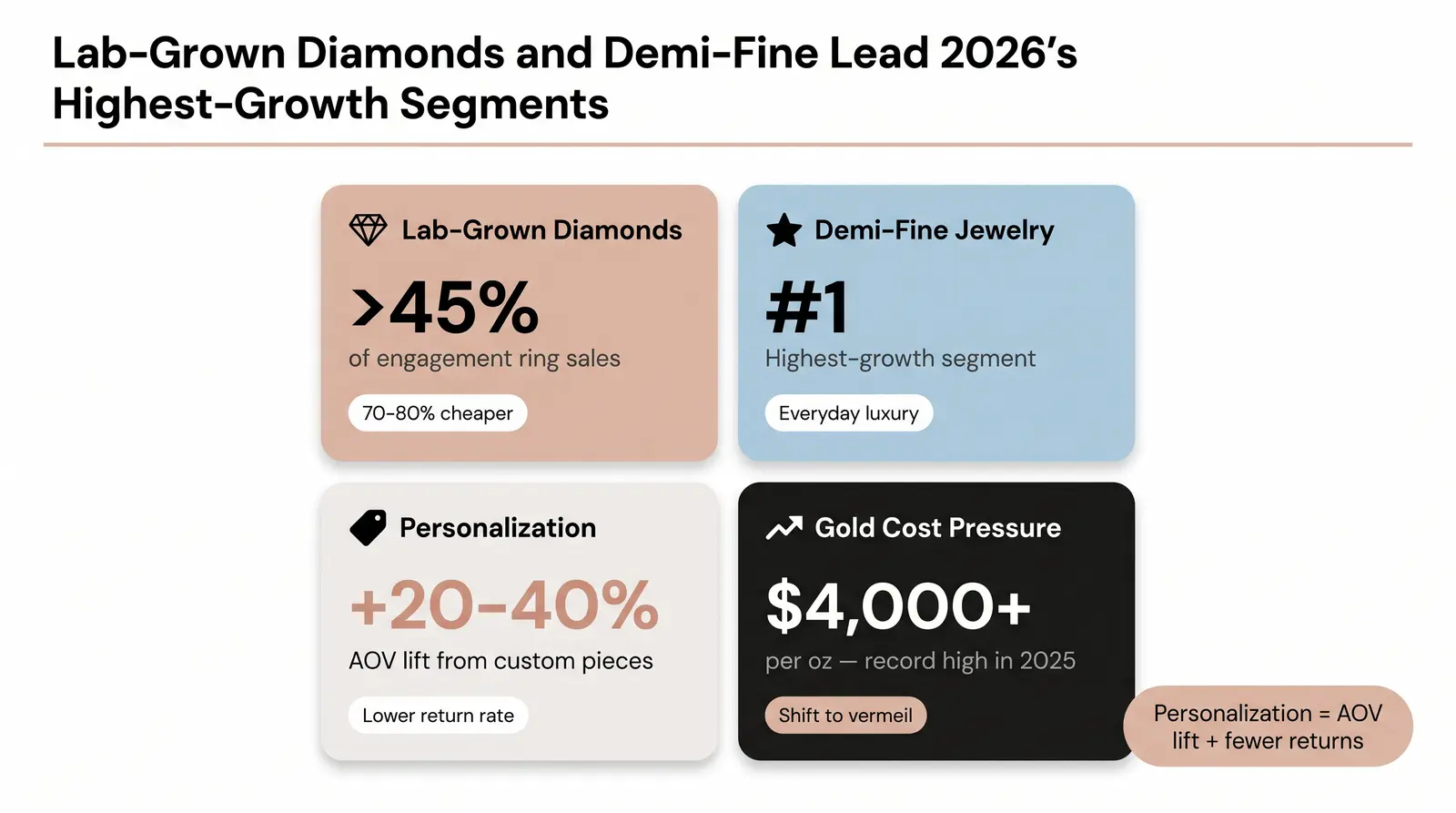

Lab-Grown Diamonds: The adoption of lab-grown diamonds is staggering. They now account for over 45% of engagement ring sales [7]. As prices have dropped (often costing 70-80% less than mined equivalents), consumers are opting for larger stones and incorporating diamonds into everyday fine jewelry, not just bridal pieces.

Demi-Fine Jewelry: Sitting comfortably between cheap fashion jewelry and expensive fine jewelry, demi-fine (typically gold vermeil or 14k solid gold with semi-precious stones) is the highest-growth segment. It appeals directly to the self-purchaser looking for durable, everyday luxury without the massive price tag.

Personalized and Custom Jewelry: Demand for personalization—name necklaces, birthstones, custom engravings—is booming. This segment commands a 20-40% AOV lift and benefits from significantly lower return rates due to the custom nature of the product [4].

Metal Cost Pressure: The most significant operational challenge in 2025–2026 is the skyrocketing cost of precious metals. Gold prices surged past $4,000 per ounce in late 2025 [11]. In response, operators are shifting strategies: reducing the weight of solid gold pieces, pivoting heavily to gold-filled and vermeil alternatives, and implementing transparent pricing models to justify necessary price hikes.

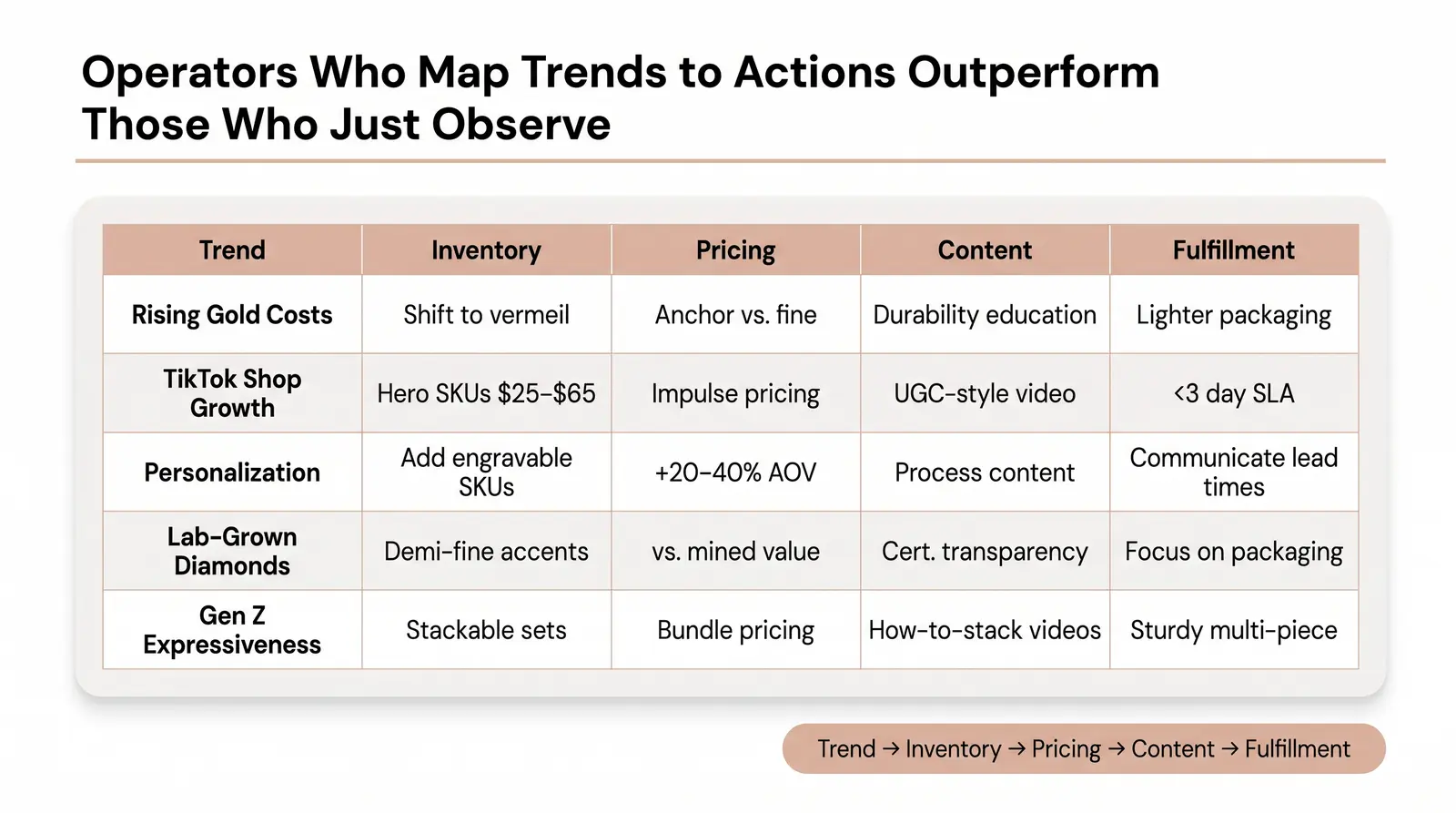

To navigate these shifts, operators need a structured approach. The Branvas Trend-to-Action Matrix™ is a four-column decision framework designed to help jewelry ecommerce founders translate macro market trends into specific, actionable operational decisions across Inventory, Pricing, Content, and Fulfillment.

The Branvas Trend-to-Action Matrix™

| Market Trend | Inventory Decision | Pricing Decision | Content Decision | Fulfillment Decision |

|---|---|---|---|---|

| Rising gold/silver costs | Shift toward gold-filled or vermeil; reduce SKU count in solid gold | Price anchor against fine jewelry; communicate material quality clearly | Educate on gold-filled vs. gold-plated; durability content | Consider lighter packaging to offset cost |

| Social commerce growth (TikTok Shop) | Stock high-visual, low-price-point hero SKUs for discovery | Price for impulse ($25–$65 range for top-of-funnel social) | Short-form UGC-style video content; haul-ready packaging | Fast fulfillment SLA critical; <3 days expected |

| Personalization demand | Add engravable or birthstone variants to core SKUs | AOV lift of 20–40% justified; price accordingly | Show the customization process; build anticipation content | Longer lead times — communicate clearly at checkout |

| Lab-grown diamond adoption | Consider lab-grown diamond accent pieces in demi-fine line | Price vs. mined diamond alternative; communicate value clearly | Trust and education content; certification transparency | No special fulfillment requirement; focus on packaging |

| Gen Z expressiveness | Stackable sets, chunky statement pieces, colorful enamel | Bundle pricing to increase AOV | Styling content; "how to stack" videos | Multi-piece orders — sturdy packaging matters |

Using this matrix allows founders to move from passive observation to active strategy. For example, if you see gold costs rising, you don't just accept lower margins; you actively adjust your inventory toward vermeil, update your pricing architecture, educate your customer through content, and optimize fulfillment costs.

If you're building a jewelry brand and want to apply this framework without sourcing, branding, and fulfillment complexity holding you back, Branvas's How It Works page walks through exactly how we support founders at each stage.

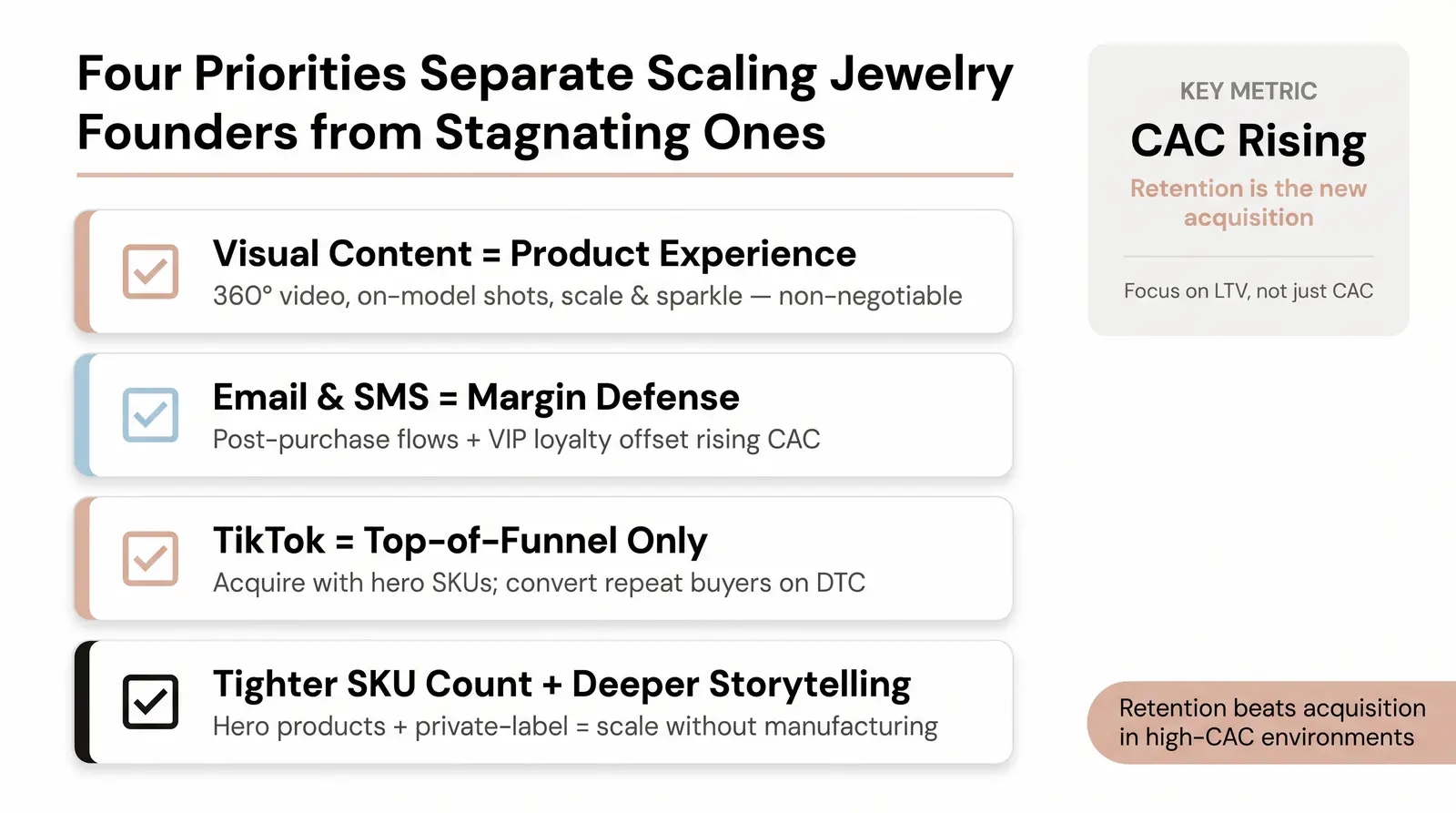

For independent jewelry founders operating on Shopify, 2026 requires a focus on operational efficiency and trust-building.

First, visual content is no longer just marketing; it is the product experience. High-quality product photography, 360-degree video, and on-model shots are table stakes. If a customer cannot clearly see the scale, drape, and sparkle of a piece, they will not convert.

Second, email and SMS retention are your primary margin defenses. With customer acquisition costs (CAC) rising across paid social, the profitability of a jewelry brand relies heavily on repeat purchases. Building robust post-purchase flows and VIP loyalty programs is essential.

Third, treat social commerce (like TikTok Shop) as a top-of-funnel discovery channel, not your primary profit center. Use it to acquire customers with lower-priced hero SKUs, and then migrate them to your DTC site for higher-margin, repeat purchases.

Finally, in a high metal-cost environment, a tighter SKU count with deeper storytelling is far more effective than a bloated catalog. Focus on hero products that define your brand aesthetic. For scaling founders who want to focus on marketing and community building rather than managing production and fulfillment logistics, private-label partnerships are becoming the standard operating model.

Branvas is built for exactly this stage — founders who know their customer but don't want to be manufacturers. See how Branvas works for ecommerce sellers →

1. What is the current size of the jewelry ecommerce market in 2025–2026?

The global online jewelry market is projected to reach approximately $85.7 billion in 2026, growing at a compound annual growth rate (CAGR) of roughly 13%. Online sales now account for about 25% of total global jewelry purchases, reflecting a permanent shift in consumer comfort with buying high-value items digitally.

2. What is a good conversion rate for a jewelry ecommerce store?

The global average ecommerce conversion rate for the luxury and jewelry category is between 1.19% and 1.5%. However, "good" depends on your segment. Fashion jewelry stores should aim for 2.5% to 4.5%, while fine jewelry stores operating at much higher price points typically see healthy conversion rates between 0.5% and 1.0%.

3. How is social commerce changing jewelry buying behavior?

Social commerce, led by platforms like TikTok Shop and Instagram, has fundamentally shifted product discovery. It has compressed the funnel for lower-priced fashion jewelry, allowing consumers to discover and purchase within the same app. For fine jewelry, social platforms act as critical trust-building and aesthetic curation channels before the customer moves to a DTC site to complete the purchase.

4. Are lab-grown diamonds affecting the broader jewelry ecommerce market?

Yes, significantly. Lab-grown diamonds now account for over 45% of engagement ring sales in the U.S. Because they cost substantially less than mined diamonds, they are democratizing access to larger stones and driving growth in the demi-fine and everyday fine jewelry segments, forcing traditional retailers to adjust their pricing and inventory strategies.

5. What AOV should a jewelry ecommerce store target to be profitable?

Profitability depends on your Customer Acquisition Cost (CAC) and margins, not just AOV. However, industry benchmarks show fashion jewelry averaging $40–$85, demi-fine averaging $85–$250, and fine jewelry averaging $500+. Brands should focus on increasing their specific AOV through bundling, personalized upsells, and tiered pricing strategies to offset rising acquisition and material costs.